How Much of ERCOT's 69.7 GW Gas Queue Can You Actually Contract?

For hyperscalers pricing offtakes, infra funds underwriting platforms, and developers valuing queue positions: a transparent way to discount headline nameplate down to deliverable megawatts.

For hyperscalers · For infra funds · For developers · ercot · gas · deliverability · underwriting

Tafel Power · July 11, 2026 · 4 min read

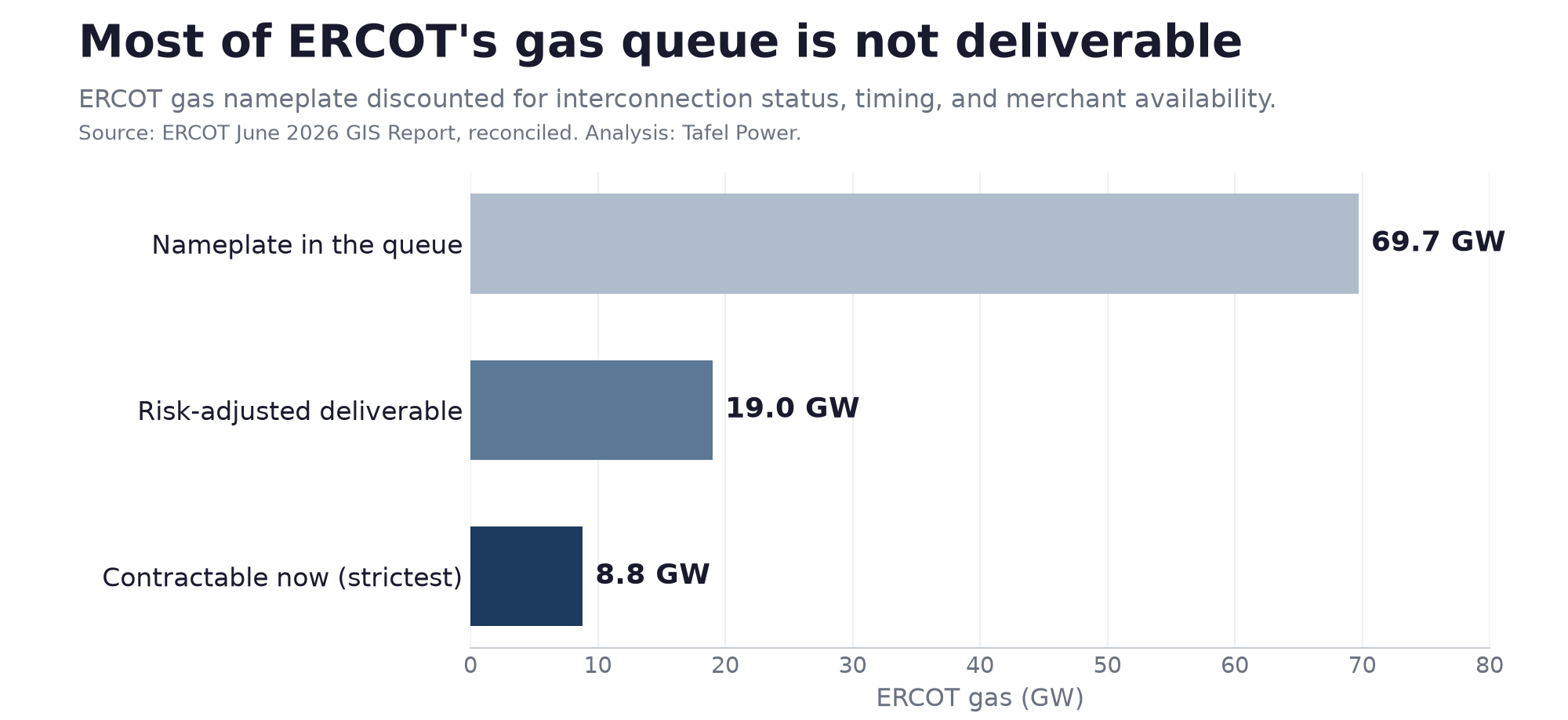

Every firm-power conversation in ERCOT starts with a nameplate number, and nameplate is the least useful figure in the market. The gas queue reads 69.7 GW. That is a list of study requests, not a supply curve, and everyone already knows to discount it. The problem is that everyone discounts it privately, with their own numbers, in a way no counterparty can check. This piece publishes a method anyone can apply and dispute.

Three discounts

Translate a project's nameplate megawatts into deliverable megawatts by applying three transparent factors. Each is a number a counterparty can inspect.

| Factor | Setting | Multiplier |

|---|---|---|

| Interconnection status | Signed interconnection agreement | 1.0 |

| Study advanced, no agreement | 0.5 | |

| Study underway, no agreement | 0.25 | |

| In-service timing | 2026 to 2027 | 1.0 |

| 2028 | 0.85 | |

| 2029 or later | 0.6 | |

| Merchant availability | Merchant developer | 1.0 |

| Cooperative, municipal, or public authority | 0 |

Multiply the three. The result is risk-adjusted deliverable megawatts: nameplate weighted by how likely a project is to connect, when it can come online, and whether a merchant buyer can contract it at all.

Applied to the June 2026 ERCOT gas queue

Run every gas project through the three factors and the 69.7 GW of nameplate becomes about 19 GW of risk-adjusted deliverable capacity, 27 percent of the headline. The stack is 14.6 GW signed, 1.9 GW with a completed study but no agreement, and 53.3 GW still in study. Two things drive the discount. Almost none of the unsigned gas has completed its study, so that 53 GW sits at the 0.25 setting. And most of the unsigned pool also carries a 2029-or-later date, which compounds the timing factor. The signed capacity, by contrast, is mostly near-term and survives the discount.

Set the same factors to a pass-fail filter, full credit only for signed, merchant gas online by 2028 and zero for everything else, and the number is 8.8 GW. That is the same figure as the deliverable-set analysis: not a separate method, just the strictest setting of the same three discounts.

The two numbers answer different questions. 8.8 GW is a floor a buyer can contract against today. 19 GW is a probability-weighted expectation across the whole queue, not a set any single buyer can sign, since no one project is 0.25 deliverable. The number a buyer can realistically assemble sits between them, and it is not the 69.7 GW headline.

The factors are judgment, and that is the point

The factor values are Tafel Power's estimates, not observed frequencies, and they are meant to be adjusted to a user's own risk tolerance. A conservative underwriter can set the study-underway factor to 0.15 and the 69.7 GW becomes about 15 GW. A more generous one can set it to 0.35 and get about 21 GW. The merchant factor is the most aggressive assumption: a hard 0 on cooperative, municipal, and public-authority gas says a merchant buyer cannot contract it, not that the megawatts do not exist, and relaxing it toward 0.3 would raise the figure. Across every setting here, from the 21 GW generous case to the 8.8 GW contractable-now floor, nameplate overstates deliverable capacity by three to eight times. What publishing the factors removes is the ability to hide the discount.

What this changes for each user

Hyperscaler energy leads. Price offtakes against risk-adjusted deliverable megawatts, not nameplate. This gives a defensible denominator for a competitive process and a number you can put in front of a counterparty without it being dismissed as a private guess.

Infra funds. Underwrite a gas platform on its risk-adjusted deliverable capacity, and stress the factors rather than the nameplate. A platform whose value rests on 2029-plus, unsigned megawatts is worth a fraction of its stated pipeline under any reasonable setting.

Developers. The method prices exactly what you hold. Moving a project from study-underway to a signed agreement, or from a 2029 date into the near-term window, is a step change in risk-adjusted value, and the discount shows how large that step is.

Methodology

Figures are reconciled from the ERCOT June 2026 GIS Report (Large and Small Gen, projects with a Full Interconnection Study requested) against that immutable source file. Interconnection status is read from the report's IA Signed field and GIM Study Phase; in-service timing from the projected commercial operation date; merchant availability by excluding cooperatives, municipal utilities, and public authorities. The factor values are Tafel Power's judgment, published so they can be inspected and adjusted, not an ERCOT-published category, and the 19 GW and 8.8 GW figures are outputs of the method, not ERCOT figures. Figures reflect the June 2026 snapshot and may have changed since.

All data compiled by Tafel Power from public sources. Framing informed by the firm's transaction advisory work in ERCOT and cross-ISO markets.

For discussions on ERCOT and cross-ISO power transactions, large-load diligence, or AI infrastructure power strategy: kris@tafelpower.com

More from Insights

The Second-Largest Merchant Firm-Gas Queue Is in the Plains

For hyperscalers · For developers · spp · gas · oklahoma

July 10, 2026 · 1 min read

For data centers willing to look past the marquee markets: SPP holds more deliverable firm gas than PJM and MISO combined, mostly in Oklahoma and the Texas Panhandle.

Firm Gas in ERCOT Is a Fifteen-Counterparty Market

For hyperscalers · For infra funds · ercot · gas · procurement

July 9, 2026 · 3 min read

For hyperscalers and infra funds procuring firm power: when the deliverable set sits in a countable number of sellers, price is set by relationship and option value, not by an auction.